PortiFiPortiFi product overview

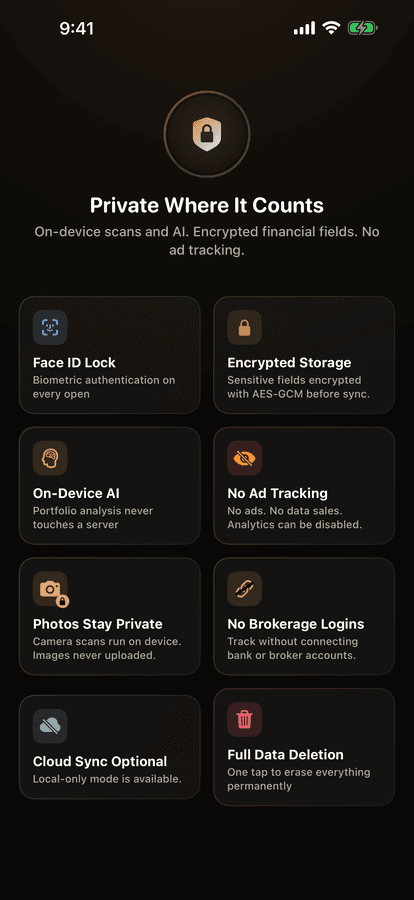

How data gets inManual-first entries, screenshot and scan workflows, plus read-only public wallet lookup. Bank or brokerage credentials are not required.

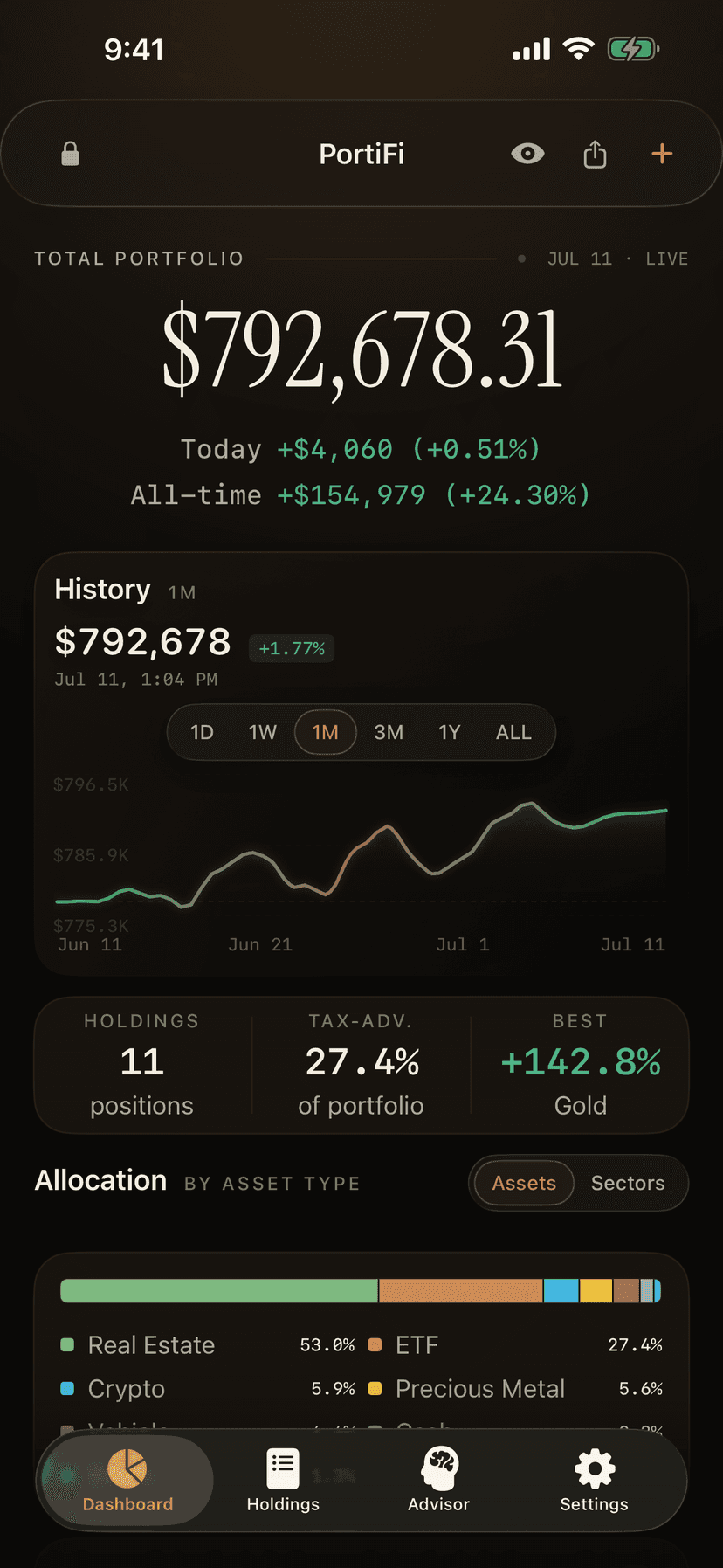

CoverageStocks, ETFs, crypto, real estate, vehicles, collectibles, cash, debt, metals and retirement assets.

TradeoffMore user control and broad manual coverage, with less automatic account syncing.

Best fitInvestors who prioritize privacy and need one view across market and real-world assets.